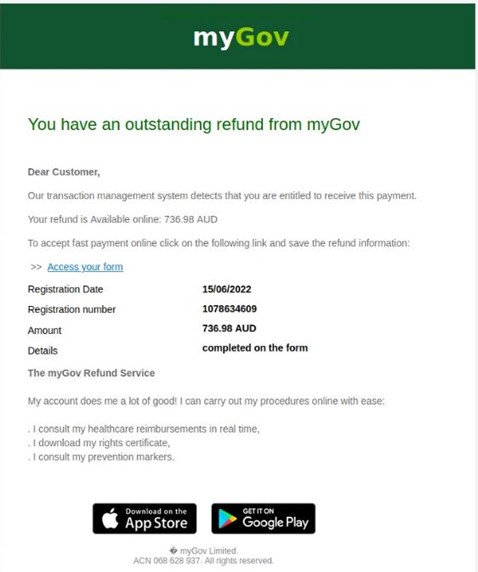

The ATO has cautioned taxpayers to be aware of phishing email scams in the lead up to this tax time.

These phishing emails tell recipients that their ‘2022 tax lodgement’ has been received. The email also asks recipients to open an attachment to sign a document and complete their ‘to do list details’. These emails are not from the ATO — the ATO has advised that if you do get an email like this, do not click on any links or open any attachments. The ATO advises you to forward the email to ReportEmailFraud@ato.gov.au, and then delete it.

The ATO also provides the following tips:

The real ATO will never send an email or SMS with a link to log in to their online services.

The ATO may use email or SMS to ask you to contact them, but they will never send an unsolicited message asking you to return personal identifying information through these channels.

If you think a phone call, SMS, voicemail or email claiming to be from the ATO is not genuine, do not reply to it. Instead, you should either phone the ATO on 1800 008 540 or go to Verify or report a scam to see how to spot and report a scam.

- 130x100")