DIVISION 296 TAX

Legislation introducing a new tax on superannuation earnings for individuals with total super balances above $3 million has been enacted by Parliament. . At the time of writing, we are still waiting for the accompanying regulations to be released. The regulations will provide further detail on how the rules will operate in practice.

We’ve summarised the new legislation and what it means for you.

When will the rules apply?

These rules will begin on 1 July 2026, with the first assessments on 30 June 2027.

During the first year, transitional rules will apply where the calculation and the assessment will be based solely on your 30 June 2027 total super balance.

After the first year, the assessment is based on the higher of your total super balance at the start or end of the financial year.

You will have until 30 June 2027 if you wish to withdraw from super to reduce your total super balance to $3m or $10m (and you have satisfied a condition of release). We recommend you seek advice before making this decision.

What earnings will the tax be applied to?

This tax will only apply to realised earnings being realised at fund-level including interest, dividends, rent, and actual capital gains. Unrealised gains are excluded.

Div296 earnings will be applied to the fund’s taxable earnings minus assessable contributions, plus exempt pension income.

What is the tax?

- The tax is pro-rated, meaning only the portion of earnings attributable to the balance above each threshold is taxed.

- You as an individual will be assessed and tax is payable by you. You will have the option to pay it either yourself or withdraw the tax from your super fund.

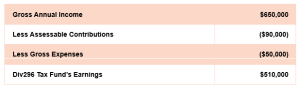

Example: Div296 Fund Earnings where member is in Accumulation and Pension Mode.

James Street Super Fund has gross annual income of $650,000, including $90,000 of assessable contributions, and $50,000 in gross expenses. 33.3% of the fund’s income is exempt from income tax.

For Div296 tax, earnings are calculated as follows:

In summary, the tax-exempt income due to the pension, is irrelevant for the calculation of Div 296 tax.

Example: Div296 Fund Earnings where members are entirely in Pension Phase.

Eagle Street Super Fund has two members who are entirely in pension phase. The fund received $200,000 of unfranked income and $750,000 in gross discounted capital gains from asset disposals. There are $50,000 in gross expenses.

The capital gain is disregarded, as the fund is essentially 100% in pension phase. Eagle Street SMSF’s taxable income will be $nil.

A modified calculation of the capital gains is required to calculate the Div296 Earnings.

Net capital gain (1/3 discount applied) = $750,000 ÷ 3 x 2 = $500,000

Fund Earnings for Div296 Tax = $500,000 + $200,000 – $50,000 = $700,000

In summary, although the capital gain is disregarded for income tax purposes, it is included in Div 296 earnings.

What are the total super balance thresholds?

The total super balance will be a two-tiered assessment.

- Up to $3 million total super balance: No additional tax and normal super fund tax applies (typically 15%)

- $3 million–$10 million: Additional 15% (totalling 30%)

- Above $10 million: Additional 25% (totalling 40%)

As noted above, from 1 July 2027, the assessment is based on the higher of your total super balance at the start or end of the financial year.

Example: Total super balance greater than $3mil

Adelaide has a total super balance (TSB) of $4mil at 30 June 2027. In the same year her total super earnings are $100,000. As Adelaide’s TSB is over the threshold of $3mil and the super fund has earnings, Adelaide will be assessed under Div296 Tax.

Proportion above the $3m threshold: ($4,000,000 – $3,000,000) ÷ $4,000,000 x 100 = 25%

Taxable earnings: $100,000 x 25% = $25,000

Division 296 Tax levied: $25,000 x 15% = $3,750

Adelaide’s Division 296 liability is $3,750 for the 2026/27 financial year.

Example: Total super balance greater than $10mil

Paul has a TSB of $12mil at 30 June 2027. In the same year his total super earnings are $500,000. As Paul’s TSB is over the threshold of $3mil and has total super earnings, Paul will be assessed under Div296 Tax.

Paul’s Division 296 liability is $64,585 ($56,250 + $8,335) for the 2026/27 financial year.

Will there be any indexation applied to the thresholds in future years?

Both the $3 million and $10 million thresholds will be indexed annually to CPI (in increments of $150k and $500k respectively), mitigating bracket creep.

Will there be any cost base adjustments available?

A cost base adjustment will be available to all asset owned as at 30 June 2026. An election must be made in the first year (this being the 2026/27 financial year). The election is applied on a blanket basis and can’t be chosen asset‑by‑asset. Planning and modelling are important, as some assets may have significant unrealised losses, which you may not want to forfeit through a cost base adjustment.

How can you plan for this tax?

- Valuations: Essential for accurate balance measurement and earnings attribution for cost base adjustments. If a valuation is provided as a range, you might want to consider valuing at a lower range.

- Equalise your member balances: for example withdrawals and recontributions or spouse splitting concessional contributions.

- Retirement strategies: Members may choose to adjust contributions or withdrawals to manage exposure to Division 296.

- Segregation and restructuring across accounts/funds may mitigate tax impact.

What action is needed before 30 June 2026?

- Understand your unrealised capital losses when considering cost base adjustments

- Review your investments and identify any unrealised capital losses. Realising these losses prior to 30 June 2026, may help minimise your Div 296 tax in the future. Seek advice from your accountant and financial advisor to assist you with this decision.

- Organise accurate valuations

- Get market valuations for all SMSF assets as at 30 June 2026.

- Use independent valuers for property and reliable sources for all investments to ensure these are acceptable for audit.

What else can you do to prepare?

- Cost Base Adjustment

- Undertake planning and modelling to determine whether making a cost base adjustment election could be beneficial to you, including if you anticipate that Div 296 tax will apply to you at any stage in the future.

- Review and understand election process – the ATO will provide further details. We understand that the deadline is to be aligned with your 2026/27 SMSF annual return.

- Review/Update SMSF Records

- Keep accurate cost base records for adjusted cost base purposes.

- Ensure your accountant and auditor have updated figures.

Keep supporting documentation for audit and future compliance purposes, especially market value record.